Liquid (Re)Staking Native

Or derivatives of otherwise illiquid tokens

Introduction

In Proof-of-Stake (PoS) blockchains, those who want to validate transactions need to lock up some of the native tokens for a while. They get it back when they're done with their job. However, during the staking period, these tokens remain illiquid and are ineligible for trading or being used as collateral.

Upon the launch of Ethereum's Beacon chain, which enabled users to stake 32 ETH to assume the role of validators, there was a surge in interest from individuals eager to accrue additional ETH through validation rewards. Unfortunately, the validator queue often extended to substantial waiting periods, at times reaching 45 days before one could attain the status of an active Ethereum validator. Without achieving active validator status, one would not be entitled to validation rewards, and liquid staking protocols were introduced to overcome this challenge.

The realm of liquid staking is rapidly evolving and is anticipated to become a prominent topic within the DeFi landscape. Nevertheless, there exists a significant degree of ambiguity surrounding the terminologies and concepts within this domain.

As a response to this challenge, this article seeks to provide an encompassing overview of this narrative while placing a special emphasis on the prospective developments and advancements in the associated protocols.

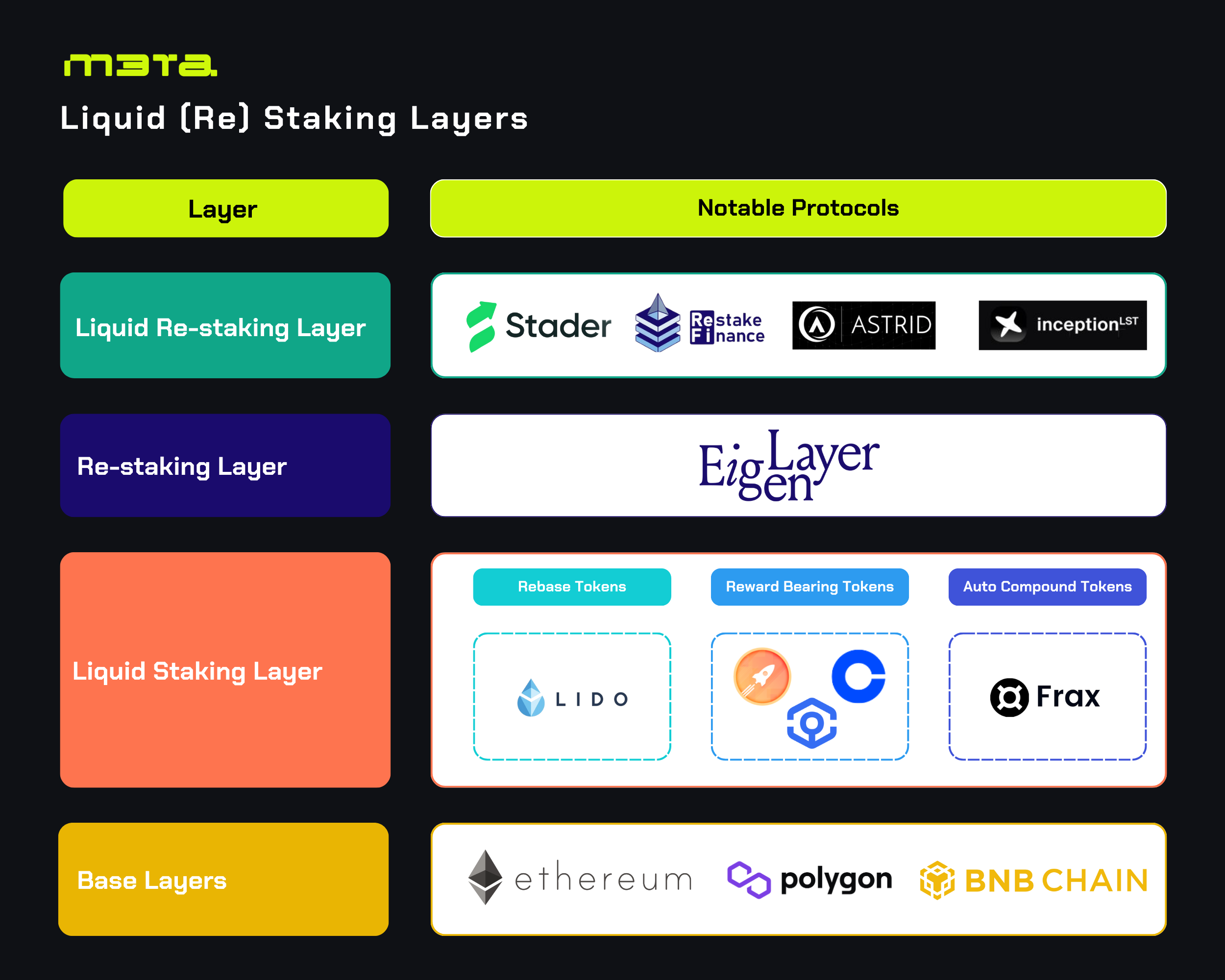

Layers Breakdown

Base Layers

Base layers are any PoS blockchains that permit users to become validators by staking a fixed amount of the native token. It's worth noting that there are PoS blockchains that exclusively authorize trusted third parties to serve as validators; such blockchains are not categorized as base layers. This article will primarily concentrate on Ethereum and associated protocols developed atop Ethereum for the sake of simplicity.

Liquid Staking Layers

Liquid staking layers represent protocols that provide liquid staking services, allowing for the provision of liquidity to staked assets, making staked assets, such as ETH, tradable and transferable.

Liquid staking protocols introduce a novel tokenization mechanism, giving rise to Liquid Staking Tokens (LSTs), which are derivative representatives of the underlying assets. In essence, both Liquid Staking Tokens (LSTs) and Liquid Staking Derivatives (LSD) refer to the same concept. These LSTs can be traded or utilized as collateral, much like other ERC-20 tokens.

To illustrate the operation of LSTs in conventional financial terms, consider the analogy of a certificate of deposit. Suppose you have $1,000 deposited in a savings account. The funds are recorded in your passbook, and you must wait until maturity to access your money, rendering them illiquid during the deposit period. Alternatively, if you invest the same $1,000 in a certificate of deposit, it can serve as collateral, typically referred to as a CD-Secured Loan, or be traded in the secondary market as Brokered CDs. Liquid staking tokens operate in a manner similar to certificates of deposit, effectively unlocking liquidity for assets that would otherwise remain illiquid.

There are three primary types of Liquid Staking Tokens:

Rebase tokens: These tokens progressively increase in quantity as rewards accumulate. Holders of rebase tokens witness their balances adjust automatically, with stETH by Lido serving as an example.

Reward-bearing tokens: These tokens maintain a constant quantity, while the value of the liquid staking token increases. Most LSTs in the market fall under this category, including rETH (by Rocket Pool), cbETH (by Coinbase), and ankrETH (by Ankr).

Auto-compounding tokens: Holding these tokens grants a percentage claim on an increasing portion of the vault's underlying assets.

Unlocking the liquidity of staked assets holds a significant advantage for participants in the staking ecosystem, offering the potential for yield from both staking activities and DeFi endeavors. Since liquid staking tokens adhere to the ERC-20 standard, they can be seamlessly integrated into various DeFi protocols, including lending pools, decentralized exchanges, and prediction markets. This expansive integration opens up a world of possibilities for earning yield and engaging in a diverse array of financial activities.

In practice, users can explore rehypothecation (when a lender re-uses the collateral posted from one loan to take out a new loan) to generate additional income. This entails staking ETH in a liquid staking protocol, receiving LSTs tokens, using these LSTs as collateral to borrow ETH, and repeating the process iteratively. This approach can be combined with Liquid Re-staking, a concept we will delve into later, to further enhance yield by redirecting staked ETH.

Re-staking Layer – EigenLayer

EigenLayer serves as a middleware protocol that introduces the concept of restaking, which empowers users who stake ETH on native or liquid staking platforms to reinforce the security of other protocols. Restaking leverages staked ETH to safeguard a variety of other protocols on Ethereum.

EigenLayer emerges as a security-as-a-service platform that addresses the problem of high costs associated with establishing validator networks faced by new protocols built atop of Ethereum. By joining EigenLayer, Ethereum validators get extra reward from the networks that they provide security for.

There are two key ideas behind how EigenLayer operates: pooled security through restaking and an open marketplace.

Pooled security means that the EigenLayer protocol gathers security from users and validators who are involved in restaking. Ethereum validators can choose to connect their staked ETH to EigenLayer and select which network using EigenLayer they want to help secure.By doing this, validators start providing security through EigenLayer's restaking feature.

However, there's a catch: if a validator doesn't do their job properly, the network they're helping can reduce the amount of ETH they earn. This risk applies to both the validator and the network.

The second part of how EigenLayer works is the open marketplace.

The open marketplace is a marketplace where networks and validators can choose how they use EigenLayer's security. Validators can pick which networks match their risk and reward preferences. Networks can decide what kind of ETH validators they need to have before they can join the network.

For instance, a network might only allow validators who use regular ETH for restaking and not LSTs such as stETH or rETH. Each network can also set specific requirements for validators, for example, only allowing validators who are experienced with DEX validation. Additionally, networks can integrate their own native tokens into the transaction validation process, making the security even more robust.

Liquid Re-staking Layers

“LRTs are to restaking what LSTs are for staking.”

Liquid re-staking tokens (LRTs) serve as derivatives of liquid staking tokens, offering additional functionalities that enable liquid re-staking protocols to repurpose the underlying token, thereby bolstering security for multiple networks. EigenLayer stands as a pioneering force in the realm of liquid re-staking, with LRTs (currently support stETH, rETH, & cbETH ) acting as proxies for assets staked through EigenLayer's re-staking contract.

LRTs deliver comparable advantages to LSTs, such as enhanced liquidity and flexibility. Both LSTs and LRTs are structured around core assets, typically native blockchain tokens, introducing participants to additional avenues for achieving higher yields.

Beside those, users can gain exposure to a variety of protocols, each offering distinct yield potentials. This heightened diversification significantly increases the odds of users benefiting from airdrops in these protocols.

The advent of liquid staking, alongside the emergence of liquid re-staking, represents the next innovative milestone in the DeFi space. This shift is spurred by a perceptible slowdown in the current DeFi landscape, attributed in part to the 2022 market crash. Users are increasingly recognizing that token staking in DeFi serves more as a mechanism to curb token inflation than to provide tangible benefits to holders.

Furthermore, many projects now offer diminished yields compared to the DeFi heyday of just two years ago when DeFi yields could reach five-figure numbers. In this context, holding derivatives of blue-chip tokens is increasingly seen as a more prudent investment strategy, offering similar returns with reduced risk.

How to Get Started with LSTs and LRTs

For those seeking additional ETH yield or exploring novel DeFi strategies, this section provides a concise guide to navigate this space.

To start, deposit native tokens to one liquid staking protocol and receive LSTs. These LSTs serve as collateral to secure additional ETH, effectively engaging in the rehypothecation process as previously mentioned.

Alternatively, you can leverage LSTs as collateral to borrow various tokens for other DeFi opportunities.

A third avenue involves staking LSTs within liquid re-staking protocols to mint LRT, which can then be used as collateral for further token borrowing. It's worth noting that both LST and LRT are tradable on secondary markets, offering liquidity when required or when transitioning away from ETH positions.

Notable Liquid Staking Projects

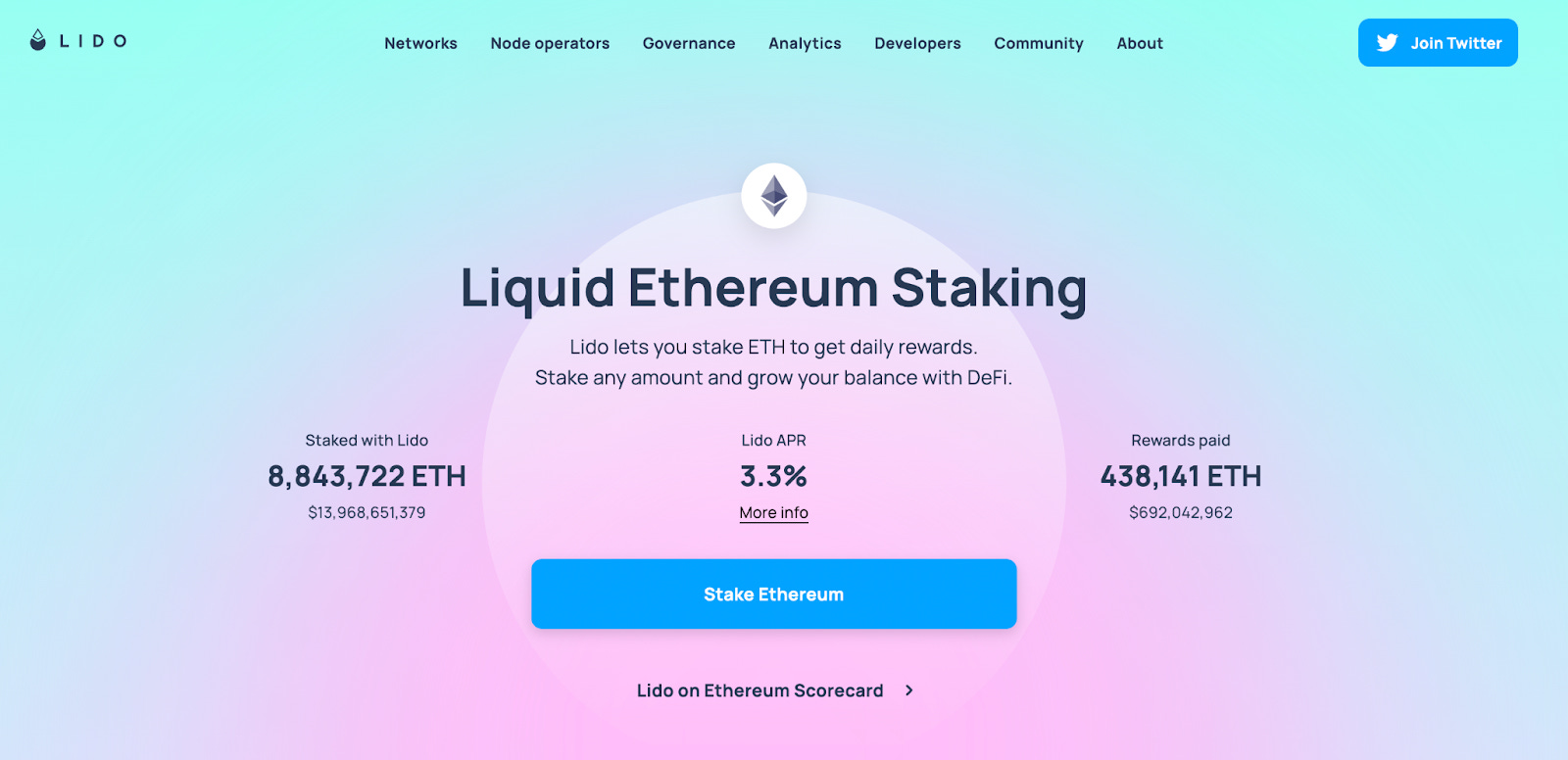

Lido Finance is a liquid staking solution for proof-of-stake cryptocurrencies. It supports staking on Ethereum's post-Merge consensus layer, as well as other layer-1 PoS blockchains like Polygon, Kusama, Solana, and Polkadot.

Lido created ‘st-tokens’ as tokenization of the native token: stETH for ETH, stMATIC for MATIC, stDOT for DOT, and etc. stETH is a token linked 1:1 to ETH, which means you get staking rewards as additional tokens. When a user deposits 1 ETH, they get 1 stETH. Your stETH balance updates once a day when the oracle reports changes in Eth2 deposits and rewards from users staking through Lido. Instead of seeing a transaction in your wallet, your stETH balance automatically changes to reflect these rewards.

Rocket Pool is a decentralized staking protocol for Ethereum that allows users to stake ETH without having to run their own node. Instead, users stake ETH with node operators who run the necessary infrastructure.

Rocket Pool is trustless, meaning that users do not have to give up custody of their ETH. Rocket Pool also offers liquid staking, meaning that users can trade their staked ETH for rETH, which can be used in other DeFi applications.

When users deposit ETH to Rocket Pool, a proxy token rETH will be minted. rETH is fully composable in the wider DeFi landscape, while accruing value from ETH earned through staking.

Ankr is a decentralized Web3 infrastructure provider, connecting developers, decentralized apps, and stakers to various blockchains, emphasizing multi-chain tools and infrastructure nodes. Ankr makes participating in blockchain networks and staking more accessible.

ankrETH is a liquid staking token that represents Ethereum deposited on validators with all the staking rewards that it has accrued. As a reward-bearing token, the value of 1 ankrETH compared to ETH increases over time as rewards accumulate, tying its market price to the redeemable Ethereum amount and its price.

Frax Finance is a decentralized finance (DeFi) protocol that provides users with access to a variety of financial products and services.

frxETH is a token representing staked ETH on Frax validators, allowing users to benefit from staking without running a node. It's usable in DeFi apps like regular ETH. sfrxETH is a vault for frxETH. When users deposit frxETH into it, they receive an equal amount of sfrxETH. As validators earn staking rewards, more frxETH is minted and added to the vault, letting users redeem sfrxETH for a higher amount of frxETH than they initially put in.

Notable Liquid Restaking Projects*

*Note: Liquid re-staking projects mentioned in this article are in test-nest phrase.

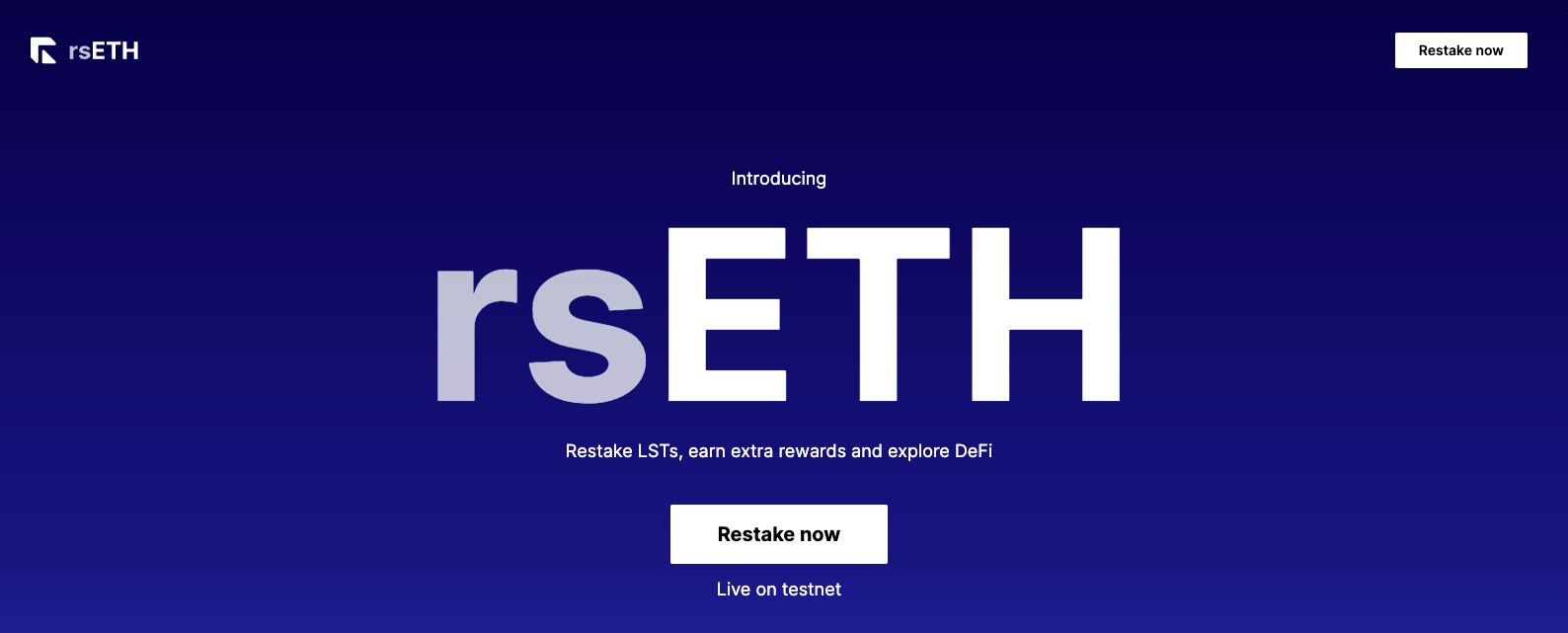

Stader Labs, a front-runner in the world of liquid staking for PoS blockchains, has made significant strides by unveiling rsETH, a liquid re-staking token.

Users can deposit eligible ETH-native LST tokens on EigenLayer to create rsETH. Supported LS tokens include stETH, rETH, and cbETH. rsETH is versatile, tradable, transferable, and usable across DeFi protocols, all while accumulating value over time through restaked points on EigenLayer.

Restake Finance simplifies the process of liquid staking on EigenLayer. Users deposit stETH and receive rstETH, which is a tokenized form of restaked Ethereum. rstETH is a yield-bearing rebasing token, allowing holders to earn EigenLayer native rewards.

InceptionLST is a Layer-2 restaking platform that boosts liquidity and yield for your staked assets. instETH is the proxy token for stETH, and inrETH is proxy token for rETH. Users deposit stETH (or rETH) to mint instETH (or inrETH). The LSTs deposited will be deployed across different pools, periodically rebalanced to streamline returns.

“Astrid Finance is the liquid restaking pool on Ethereum powered by EigenLayer. By restaking through Astrid, users are able to obtain diversification and instant liquidity for their restaking position.”

LSTs are deposited to mint Astrid liquid restaked tokens: rstETH or rrETH. rstETH is a proxy token for stETH and rrETH is proxy token for rETH. Both rstETH and rrETH are rebase tokens this mean users will see their balances adjusted automatically as rewards are accumulated.

A Word of Caution

The pursuit of higher rewards often comes hand in hand with greater risks. This holds true for the promising investment avenues of LST and LRT, which indeed offer attractive yields. However, these avenues are not without complexity and call for vigilant management. Potential investors must navigate security concerns, including safeguarding vaults and scrutinizing the integrity of smart contracts.

It's vital to acknowledge that participation in alternative networks, in the case of LRTs, inherently exposes users to third-party risks. Furthermore, despite many LSTs and LRTs being tethered to ETH, recent evidence suggests the possibility of these tokens becoming detached from this anchor. In the quest for higher returns, investors are advised to tread carefully, acknowledging both the allure and intricacies of these promising yet unpredictable investment options.

References

https://orochi.network/blog/understanding-liquid-staking-and-the-evolving-landscape

https://diadao.notion.site/The-Ultimate-Liquid-Staking-Map-985ce39dc9b8490e9b3f37b4c00119bd

https://docs.inceptionlst.com/

https://www.staderlabs.com/blogs/understanding-rseth-tech-explainer/

https://www.validatorqueue.com/

https://astrid.finance/

https://www.restakefinance.com/

Disclaimer

The views expressed herein are for informational purposes only and should not be considered as investment advice. They may not necessarily represent the opinions of M3TA. As every investment and trading opportunity carries risk, you should conduct your own research before making any decisions. M3TA assumes no responsibility for our users' investment activities or their profits or losses. The articles, data, and content provided by M3TA should not be relied upon for any investment-related decisions. We do not advise investing funds you cannot afford to lose.

This article, encompassing text, data, content, images, videos, audio, and graphics, is presented for informational purposes only and is not intended for trading purposes. M3TA cannot guarantee the accuracy, comprehensiveness, or timeliness of the content, documents, data, materials, or website pages accessible through any service, and neither M3TA nor any of its affiliates, agents, or partners shall be liable to you or anyone else for any loss or injury caused in whole. The content available through this website is the property of M3TA and is safeguarded by copyright and other intellectual property laws. Failing to provide proper citation may result in being accused of plagiarism.

Loved it, hits the bullseye.

Loved it, hits the bullseye.